When you pick up a prescription for a generic drug, you probably assume it’s covered. But have you ever wondered why your insurer covers one generic and not another-even if they’re both the same active ingredient? It’s not random. It’s not arbitrary. It’s a calculated, data-driven process that happens behind the scenes, mostly decided by teams of doctors, pharmacists, and financial analysts who sit on something called a Pharmacy & Therapeutics (P&T) committee.

What Exactly Is a Formulary?

A formulary is just a list of drugs your insurance plan agrees to pay for. It’s not a suggestion. It’s a rulebook. And for generics, that rulebook is built around one core idea: lowest cost, same effect. Most insurers use a tiered system-usually 3 to 5 levels-where generics sit at the bottom, in Tier 1. That means you pay the least. Sometimes $0. Sometimes $5. Rarely more than $15 for a 30-day supply. Compare that to brand-name drugs, which can cost $40 to $100 or more on higher tiers.The Three Rules Insurers Actually Use

P&T committees don’t flip coins. They follow three strict criteria before adding a generic to the formulary:- Clinical Effectiveness - Does it work as well as the brand? The FDA says yes, but committees dig deeper. They look at real-world studies, not just clinical trials. Did patients actually get better? Were side effects similar? If two generics are equally effective, the cheaper one wins.

- Safety - Has this generic been used by millions? Is there a history of bad reactions? Some generics, especially those made overseas, have had quality issues in the past. Insurers track adverse event reports. If a batch of a certain generic keeps showing up in ER visits, it gets pulled-even if it’s cheaper.

- Cost-Effectiveness - This is the biggest factor. A generic that costs 85% less than the brand? That’s a no-brainer. Medicare Part D plans saved $141 billion in 2019 just by pushing generics. That’s not charity. It’s math. And insurers are under pressure to keep premiums low. The cheaper the drug, the more likely it’s covered.

Why Some Generics Get Covered and Others Don’t

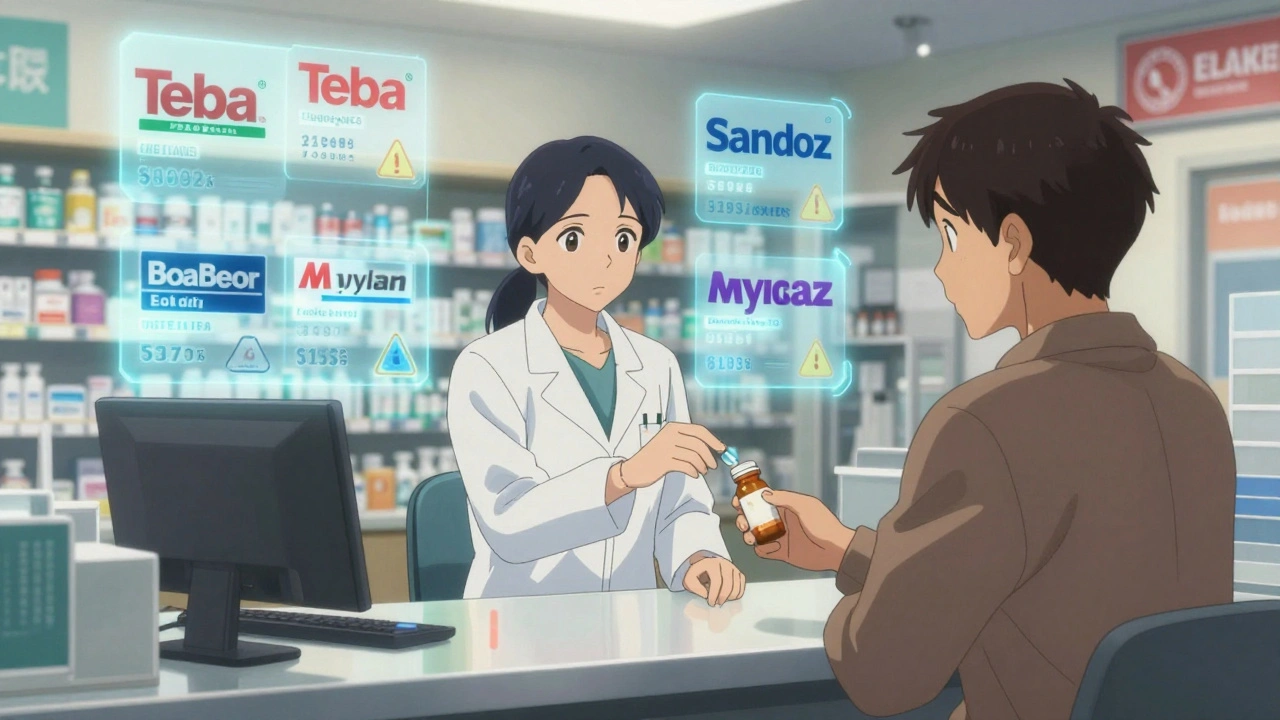

Here’s the twist: two generics with the same active ingredient can be treated differently. Why? Because insurers don’t just care about the drug-they care about the manufacturer. Teva, Sandoz, Mylan, Apotex, and Sun Pharma make about 45% of all U.S. generics. If you’re a smaller company with less market share or a history of delays, your generic might not make the cut-even if it’s FDA-approved. Insurers also favor generics that come with discounts through preferred pharmacy networks. In 2023, Medicare Part D plans started requiring pharmacies to offer deeper discounts on generics in exchange for being on their network. That means your local pharmacy might not carry the cheapest version-it’s the one the insurer negotiated with.

Therapeutic Substitution: When They Swap Your Prescription

You might not even know it’s happening. Your doctor prescribes a brand-name drug. You get to the pharmacy. The pharmacist hands you a generic. That’s therapeutic substitution. In 78% of commercial insurance plans, pharmacists are allowed to swap generics without asking you or your doctor-unless the doctor specifically says “dispense as written.” It’s legal. It’s common. But it’s not always smooth. A 2023 survey found 31% of patients reported side effects or reduced effectiveness after switching to a different generic. That’s not because the drug is bad. It’s because generics can have different inactive ingredients-fillers, dyes, coatings-that affect how your body absorbs the medicine. For some people, that tiny difference matters.What Happens When Your Generic Isn’t Covered?

If your drug isn’t on the formulary, you’re not out of luck. You can file an exception request. You need a letter from your doctor explaining why the generic you were given didn’t work-or why you had a bad reaction. The insurer has three business days to respond. If they don’t? The request is automatically approved. The Patient Advocate Foundation found that 43% of patients get denied at first. But 78% eventually get coverage after appealing. That’s a huge win. But here’s the catch: doctors spend an average of 13 hours a week just dealing with these appeals. That’s time they could spend with patients.

Yasmine Hajar

December 3, 2025 AT 18:33I used to think generics were all the same until my kid had a seizure after switching to a cheap one. Turns out the filler had corn starch and he’s allergic. Insurance didn’t care. They just wanted the lowest bid. Now I fight every single time. It’s exhausting, but someone’s gotta do it.

Jake Deeds

December 4, 2025 AT 10:00Oh wow, so insurers are just corporate vampires feeding off the suffering of the chronically ill? How novel. I’m shocked, utterly shocked. Did you also know that CEOs get bonuses for cutting drug costs? I mean, who could’ve guessed?

John Filby

December 5, 2025 AT 10:50This is actually super helpful. I never realized pharmacists could swap meds without telling you. I had that happen last month and thought I was just imagining the side effects. Now I ask ‘is this the preferred generic?’ every time. Small change, big difference.

Joe Lam

December 6, 2025 AT 23:41Let me guess-you’re one of those people who think ‘FDA-approved’ means ‘safe for everyone.’ Newsflash: the FDA doesn’t test for individual bioavailability. Your body isn’t a lab rat. Stop being naive.

Rachel Bonaparte

December 8, 2025 AT 23:26They’re not just choosing generics-they’re choosing which manufacturers to protect. Big Pharma owns the P&T committees through lobbying. Teva? Sandoz? They’re subsidiaries of the same conglomerates that make the brand-name drugs. This isn’t about cost-it’s about market control. And the FDA? They’re in bed with them too. Look up the revolving door between the agency and pharma execs. It’s not a coincidence.

They’re letting Chinese factories churn out generics with unregulated binders because it’s cheaper. Then when people get sick, the blame goes to ‘individual variability.’ Bullshit. It’s supply chain corruption wrapped in a white coat.

And don’t get me started on how insurers force pharmacies to stock only the ones with kickbacks. Your local pharmacist isn’t your friend-they’re a corporate agent. You think they’re helping you? They’re being paid to push the cheapest option, not the best one.

2025’s $2,000 cap? That’s just the opening act. Once patients are shielded from the real cost, insurers will go nuclear on generics. They’ll replace every drug with a 3-cent pill from a factory that doesn’t even have running water. And you’ll thank them for it because you won’t feel the pinch anymore. That’s the trap.

Wake up. This isn’t healthcare. It’s a financial algorithm with a stethoscope.

Scott van Haastrecht

December 9, 2025 AT 15:0878% of drug shortages are generics? That’s not a bug-it’s a feature. Insurers deliberately underfund suppliers to create scarcity. Then they jack up prices on the few remaining brands. Classic supply manipulation. The whole system is a Ponzi scheme built on patient ignorance.

And the ‘appeal process’? A joke. Doctors spend 13 hours a week on paperwork? That’s 13 hours they’re not seeing patients. That’s 13 hours they’re not billing. That’s 13 hours the system is bleeding them dry so it can keep the machine running. This isn’t broken. It’s working exactly as designed.

Chase Brittingham

December 11, 2025 AT 05:21Thanks for laying this out so clearly. I’ve been on the receiving end of this system-my dad had to switch generics three times before they found one that didn’t make him dizzy. The worst part? No one told us why the first two were pulled. It felt like playing Russian roulette with his meds.

I’m going to start asking my pharmacist the same question you mentioned: ‘Is this the preferred generic?’ I never thought to ask before. Small steps, right?

Bill Wolfe

December 13, 2025 AT 03:27Wow. Just… wow. You actually think this is about ‘saving money’? 😏 Let me introduce you to reality: the entire pharmaceutical industry is a cartel. Generics? They’re not ‘cheaper alternatives’-they’re bait. The real profit is in the ‘authorized generics’-same drug, same manufacturer, just a different label. Insurers don’t pick the cheapest-they pick the ones that pay them the biggest rebate. And guess who owns the patent? Big Pharma. 😈

And the ‘FDA-approved’ badge? That’s just a marketing sticker. The real test is whether the manufacturer has a good relationship with the P&T committee’s chair. Ever heard of ‘ghostwriting’ clinical studies? Yeah. That’s how they get on the formulary.

You think you’re getting a bargain? You’re getting a product designed to maximize corporate profit while minimizing liability. And you’re thanking them for it. 🙃

michael booth

December 14, 2025 AT 16:47Formulary decisions are grounded in evidence based pharmacoeconomic analysis. The P&T committee operates under strict guidelines to ensure therapeutic equivalence while minimizing expenditure. This is not arbitrary. It is systemic. It is necessary.

Carolyn Ford

December 15, 2025 AT 15:19Wait-so you’re saying that if I take a generic that’s not ‘preferred,’ I might get a different filler? And that could affect absorption? And no one tells me? And my doctor doesn’t even know? And this is legal? And the FDA lets this happen? And insurers don’t even disclose their criteria? And you think this is ‘not broken’? 😭

What kind of dystopian nightmare are we living in? I’m not just mad-I’m terrified. And I’m not alone. Everyone I know has had a horror story. Why isn’t this on the news? Why isn’t Congress shutting this down? Why is no one doing anything?

Martyn Stuart

December 17, 2025 AT 10:24Interesting. In the UK, the NHS has a similar system, but they’re far more transparent about their formulary criteria. Every decision is published, and manufacturers must submit full pharmacoeconomic data. We also have a national formulary-no regional variations. It’s not perfect, but at least you know why you’re getting what you’re getting.

What’s missing here is accountability. If insurers had to publish their rebate structures and manufacturer contracts, this whole system would collapse-or improve.

Jessica Baydowicz

December 17, 2025 AT 20:48Okay, but can we just talk about how wild it is that your pharmacist can swap your med without asking? Like… imagine if your mechanic just swapped your engine for a ‘cheaper version’ and said ‘it’s fine, trust me.’ Would you drive off? NO. But we do this with our bodies every day. 😳

I’m telling my doctor next time: ‘If you write ‘dispense as written,’ I’ll bring cookies.’